1. Property taxes: Real estate investors can consult the county assessor to get the exact figure for current property taxes, which could be different from what the seller lists. A buyer should also be sure to find out what property taxes they'll pay after they close escrow. It could be very different from what the seller pays. 2. Electricity: Residents usually pay for electricity. However, multifamily properties may require higher costs because of the electricity needed for common areas of the property. 3. Pest control: Pest control is mainly preventative maintenance. In the event of an infestation, the owner must intervene immediately to ensure the tenant's comfort and safety. Treatment of the average single family home can cost about $150 for a single treatment. 4. Waste management: It's the owner's responsibility to maintain cleanliness by providing trash cans and coordinating regular collection. Additionally, elevators and other shared-use areas are the rental property owner's responsibility to keep clean. An injury caused by debris in common areas is an owner liability. 5. Insurance: Insurance agents can give estimates based on the specifics of a property. Based on geography, owners may need particular coverage for events like earthquakes, floods, etc. Purchasing the right insurance is critical. 6. Homeowners Association (HOA) fees: A property manager should be able to provide information on Homeowners Association (HOA) fees. It's important to know the current fees, when the fees increase and by how much, and if there's a special assessment on the horizon. 7. Property management fees: When using a property manager, owners can expect to pay six to eight percent of the rental income toward the management fee. That figure may not include re-leasing costs following tenant turnover, which could be as high as 50 to 100 percent of a month's rent in addition to the monthly fee. 8. Vacancy: Rental properties typically won't be rented all the time, so owners should factor in some vacancies into their budget. 9. Routine maintenance: These are the expenses associated with maintaining curb appeal and common areas. This includes landscaping, cleaning, and trash and recycling collection. 10. Seasonal maintenance: Depending on location, seasonal maintenance may include pruning trees, raking and mowing, snow removal, and cleaning of gutters. Keeping away dry debris is part of fire prevention. 11. Appliance maintenance: It's in the landlord's best interest to maintain appliances themselves so that their investment is adequately taken care of. This means routinely servicing HVAC systems, sump pumps, refrigerators, stoves, washers, and dryers. 12. Emergency maintenance: Property owners should always plan for emergencies, such as a heater dying during winter, an AC giving up the ghost during a heatwave, or pipes bursting in the middle of the night. These events demand immediate attention to prevent further damage to the property and ensure the resident's comfort and safety. 13. Painting and flooring: Applying a fresh coat of paint between residents is a great way to freshen up a property. This may be the only option if an occupant left the walls particularly scuffed or marked up. If the damage exceeds normal wear and tear, a property owner may be justified in taking a percentage of the security deposit to cover the cost of repainting. But in the case of a long-term renter moving out, painting would fall under regular maintenance. Similarly, flooring may need to be replaced between residents. Carpet suffers the most from normal wear and tear. Regular carpet maintenance may include yearly professional cleaning. Owners may want to consider a flooring option that requires less care, like laminate or wood, which will speed up rental property turnover. 14. CapEx, or capital expenditure: CapEx, or capital expenditure, is a term for the costs to upgrade and improve an investment. It's used to refer to big-ticket items like the roof, water heater, and appliances. Budgeting for expected capital expenditures is easier than for surprises, since owners should know that certain items will have to be replaced periodically, they should know the lifetime of those items, and they should know their cost. Many investors set aside 5 to 7 percent of gross rental income for capital improvements (as the IRS refers to this). So, for a house that rents for $2,000 a month, the owner would want to set aside $100 to $140 a month.

0 Comments

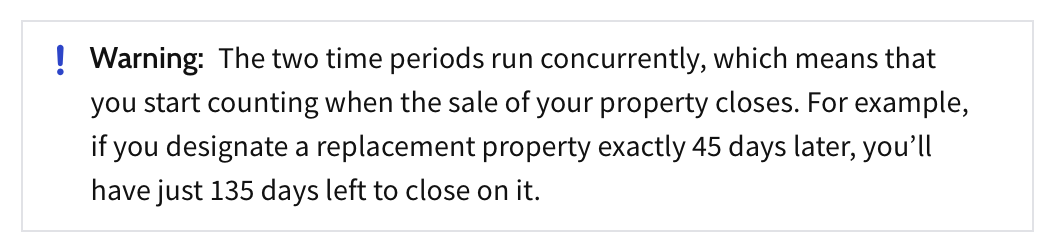

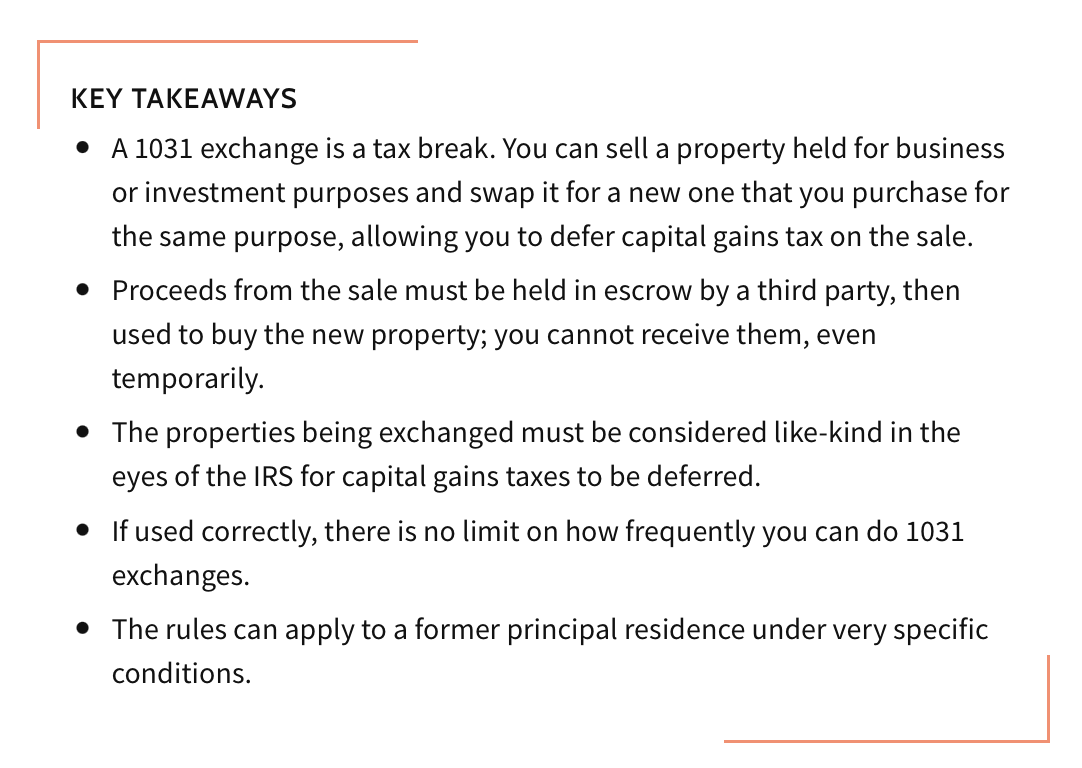

What Is a 1031 Exchange? A 1031 exchange can be complicated, but it has some big tax advantages. Here's how it works and what to remember. If you’re thinking of selling a piece of property that could result in a big profit (and a big tax bill), a 1031 exchange could be a useful strategy. 1031 exchange, named after section 1031 of the U.S. Internal Revenue Code, is a way to postpone capital gains tax on the sale of a business or investment property by using the proceeds to buy a similar property. It is also sometimes referred to as a "like-kind" exchange. What qualifies as a 1031 exchange? A key rule about 1031 exchanges is that they’re generally only for business or investment properties. Property for personal use — like your home, or a vacation house — typically doesn’t count. Securities and financial instruments, such as stocks, bonds, debt instruments, partnership interests, inventory and certificates of trust aren’t usually eligible for 1031 exchanges. How to do a 1031 exchange? A 1031 exchange can be complex, so you'll likely want to consult with a qualified tax pro. You can read the rules and details in IRS Publication 544, but here are some basics about how a 1031 exchange works and the steps involved= Step 1: Identify the property you want to sellA 1031 exchange is generally only for business or investment properties. Property for personal use — like your primary residence or a vacation home — typically doesn’t count. Step 2: Identify the property you want to buyThe property you’re selling and the property you’re buying have to be "like-kind," which means they’re of the same nature, character or class, but not necessarily the same quality or grade (more on that below). Note that property inside the U.S. isn’t considered like-kind to property outside the U.S. Step 3: Choose a qualified intermediaryIf you don’t receive any proceeds from the sale, there’s no income to tax — that’s generally the idea behind a 1031 exchange. One way to make sure you don't receive cash prematurely is to work with a qualified intermediary, sometimes called an exchange facilitator. Basically, they hold the funds in escrow for you until the exchange is complete (assuming the sale and the purchase don’t take place simultaneously). Choose carefully. If they go bankrupt or flake on you, you could lose money. You could also miss key deadlines and end up paying taxes now rather than later. Step 4: Decide how much of the sale proceeds will go toward the new propertyYou don’t have to reinvest all of the sale proceeds in a like-kind property. Generally, you can defer capital gains tax only on the portion you reinvest. So if you keep some of the proceeds, you might end up paying some capital gains tax now. Step 5: Keep an eye on the calendarFor the most part, you have to meet two deadlines or the gain on the sale of your property may be taxable. First, you have 45 days from the date you sell your property to identify potential replacement properties. You have to do that in writing and share it with the seller or your qualified intermediary. Second, you have to buy the new property no later than 180 days after you sell your old property or after your tax return is due (whichever is earlier). Step 6: Be careful about where the money isRemember, the whole idea behind a 1031 exchange is that if you didn’t receive any proceeds from the sale, there’s no income to tax. So, taking control of the cash or other proceeds before the exchange is done may disqualify the deal and make your gain immediately taxable. Step 7: Tell the IRS about your transactionYou’ll likely need to file IRS Form 8824 with your tax return. That form is where you describe the properties, provide a timeline, explain who was involved and detail the money involved. Important things to know about 1031 exchangesHere are some of the notable rules, qualifications and requirements for like-kind exchanges.

Types of 1031 exchanges Here are three kinds of 1031 exchanges to know. Simultaneous exchange In a simultaneous exchange, the buyer and the seller exchange properties at the same time. Deferred exchange (or delayed exchange) In a deferred exchange, the buyer and the seller exchange properties at different times. However, the sale of one property and the purchase of the other property have to be "mutually dependent parts of an integrated transaction." The rules here can get particularly complex, so see a tax pro. Reverse exchange In a reverse exchange, you buy the new property before you sell the old property. Sometimes this involves an "exchange accommodation titleholder" who holds the new property for no more than 180 days while the sale of the old property takes place. The Bottom Line A 1031 exchange can be used by savvy real estate investors as a tax-deferred strategy to build wealth. However, the many complex moving parts not only require understanding the rules, but also enlisting professional help—even for seasoned investors.    |